“He who sows bountifully will also reap bountifully. God loves a cheerful giver.” – II Cor. 9:6, 7.

The concept of “the circular flow of money” is pivotal to the vision of business success.

The continuous circular flow of blood in the body is pivotal to our vision for a long life. One of the health risks with which we are faced is the reduction of blood flow to our heart muscle due to the blockage of the channels through which the blood flows. We may then be medically diagnosed with atherosclerosis. There are ways to treat this disease in a timely manner so that our life span might be extended.

Similarly, investment channels facilitate the circulation of money to nurture the business trading system, where producers sell goods and services to consumers. One of the risks, with which businesses are faced, is the blockage of investment channels to the extent that they inhibit the circular flow of money. Then, the trading system may be diagnosed with “investment channel sclerosis” and, if this disease is not treated in a timely manner, our vision for business success may not be realized and our hopes for sustainable economic growth will be dashed.

MSME enterprises are fraught with a plethora of business risks associated with the corporate governance, financial, marketing, human resource development and operational business systems and hence investors may be reluctant to invest. The challenge is to reduce these risks.

Usually there is no shortage of money in the global financial system. How can we develop innovative ways of treating the “investment channel sclerosis” to maintain the circular flow of this money?

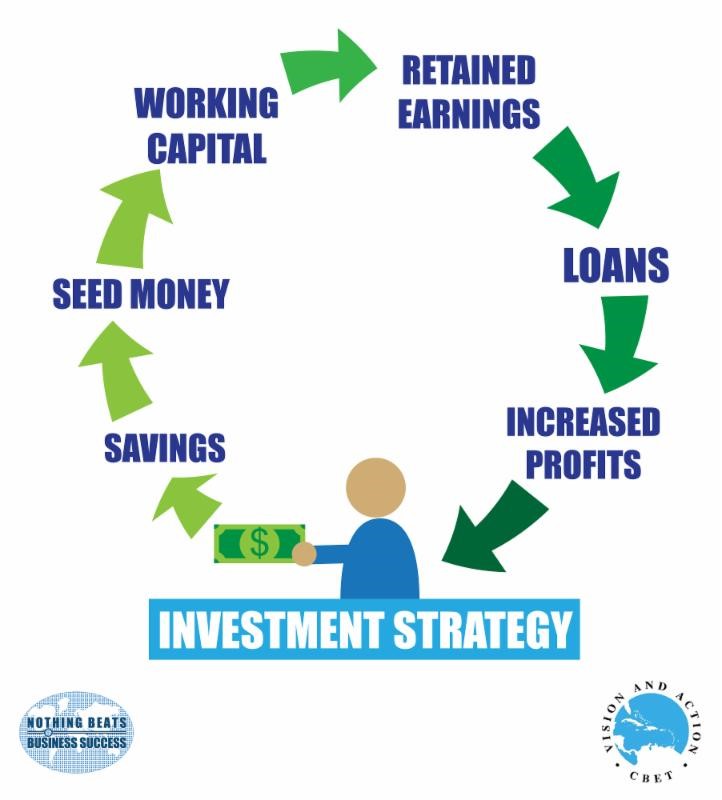

The investment channels are savings, seed capital, working capital, retained earnings, loans and increased profits. Let us consider, in turn, the following preventive and curative measures that should be employed to keep these investment channels functioning well: (1) The savings culture is best adopted at an early age and should be the first source of funds that you draw on when you start up a business; (2) Seed capital, a grant or unsecured loan, may be accessed from those who are attracted to the business model, e.g. family and friends, the private sector through corporate social responsibility and/or local, regional and international development institutions; (3) In an agricultural setting, say, Financial institutions, in particular credit unions, micro finance and development banks, may provide working capital (secured by Shepherding) for raw material purchasing, particularly when the management, credit readiness, marketing, land, operating space, equipment and labour are secure.

(4) Retained earnings should initially be ploughed back into the business based on Skip Weitzen’s principle – “Start small; Do it right; Make a profit; Then expand”; (5) Loans may usually only be considered when the business is mature enough to meet the conditions of the likes of commercial banks; and (6) Increased profits then become your ultimate investment channel and signal the advent of your financial self sufficiency.

An ingredient which ought to be embraced by all of the channels is Shepherding. The cost of the Shepherding will be out of the seed capital initially but as soon as it is viable, it will be a charge to business operations.

Let us quickly adopt a new investment strategy paradigm which recognizes that diligent Shepherding of all business systems significantly reduces business risk, making it more attractive for the investor. And, let us invest bountifully in MSME enterprises.