“I planted the seed, Apollos watered it, but God has been making it grow.” – 1 Corinthians 3:6

Professor Compton Bourne, Executive Director of Caribbean Centre for Money and Finance (CCMF), wrote an article entitled: “The Liquidity Problem in Caribbean Commercial Banks” in the CCMF’s December 2014 Newsletter: Volume 7, No. 12. In this article, he observed that “excess liquidity depresses commercial bank profitability”. Indeed, this past week a commercial bank in St. Vincent and the Grenadines, apparently without consultation with its clients, imposed a $25 per month levy on bank accounts, presumably to boost their non-interest income as a result of declining profits. The depositors are not taking it lying down and this induced a “run on the bank”.

Compton suggested that one way to address this declining profitability is for commercial banks to “become more venturesome in their search for banking opportunities within the domestic economy, expanding beyond their traditional comfort zones to finance new customers in new industries as well as in familiar industries.” This means that the commercial banks must become less risk averse or, may I suggest, look at ways of reducing the business risk associated with their customers’ proposals for finance.

My experience in dealing with start-up businesses in the Caribbean over the past 15 years is that there is no shortage of business ideas and their associated innovations which determine the core products and services of these proposed businesses. However, start-ups are perceived by commercial banks as high risk and/or as not having the required collateral. Most of these businesses, which are potential contributors to the growth of the economy, get no investment and do not see the light of day. As a result, growth in the economy is therefore commensurately impacted.

In my opinion, there is unlikely to be a change in present risk assessment practices of commercial banks so why not look at ways of reducing the business risk associated with their customers’ proposals for finance. The Shepherding component of the CBET Shepherding Model™, led by the ManOBiz™ Matrix, helps the customer to remove the obstacles along the journey to business success and reduces business risk, thus potentially increasing commercial bank business and growing the economy. When the economy wins we all win.

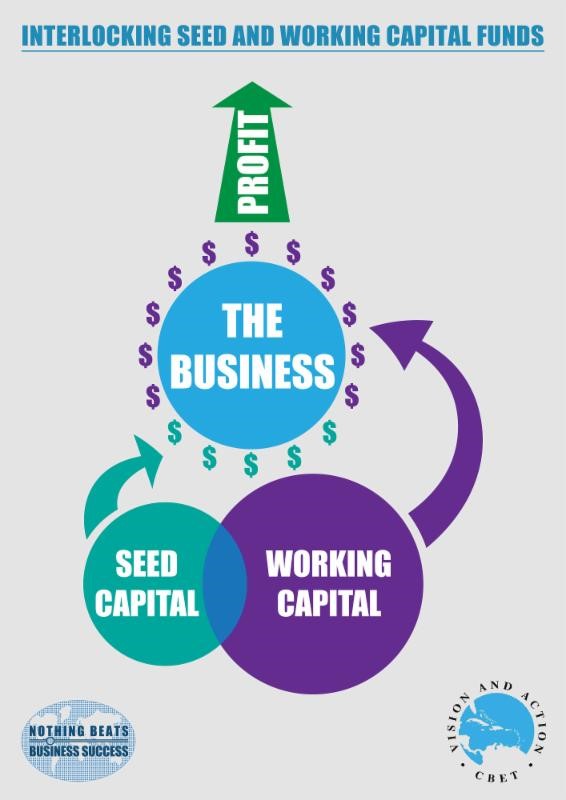

The financing component of the CBET Shepherding Model™, as depicted in the accompanying graphic, is creatively designed to pay for initial shepherding expenses through a revolving and growth seed capital fund (to start a business) and then innovatively weave the seed capital component into a working capital fund (to finance operating activities) as the business grows over time. The skillful engagement of shepherding services enhances the chances of business success and enables the commercial banks, the clients and the national economies to win.

Since change is the only constant in life, since we should recognize that practice makes improvement and that our work is never finished, let us pray that commercial banks will modify their practices and consider at least a Shepherding pilot project to build a new Caribbean – a Caribbean that is fair and just and a Caribbean where hard work and a positive attitude bring progress, fulfillment and financial prosperity for all.